When you buy a car in Malaysia, you typically have a few options to choose from when it comes to financing your purchase. If you have the means, paying the total amount with cash is the simplest way of getting things done, as it’s as uncomplicated as buying a new phone. Cash for a car, done.

However, since most people don’t have huge amounts of cash in their bank accounts (we’re not all a Bezos or a Gates), taking up a loan is the most common form of financing when buying a car. In this instance, a borrower (i.e., the car buyer) signs a deal with a lender (i.e., the bank) for an agreed-upon sum to purchase a car. In exchange, the borrower is indebted to pay back the loan amount plus interest because the lender needs to earn a profit from providing the loan.

For a majority of car buyers, a hire purchase loan is the go-to solution that helps them land a new ride. Generally, when you apply for a hire purchase loan, you can choose whether you want a fixed rate or a variable rate. But, what are the differences between the two types of car loans, and is one better than the other?

What makes up a car loan?

In a typical car loan, there are a few key aspects that are taken into consideration, namely:

- Borrowed amount: This is principal amount that the bank is willing to loan to you to purchase the car, which follows an agreed-upon margin of finance of up to 90%.

- Interest rate: Presented as a percentage, this is the profit that the bank wants to make for providing you with a loan.

- Downpayment: This is the upfront payment that covers part of the car’s cost, which is usually 10% for new cars and 20% for used cars.

- Loan period: The amount of time taken to pay off the loan, which can range from as low as one year to a maximum of nine years.

- Instalment amount: This is the amount that is typically paid monthly to the bank to clear off the loan.

The instalment amount is what most people are concerned about, and it covers both the repayment of the borrowed amount and interest charged. It’s important to note that with hire purchase loans, the bank is actually in “possession” of your newly-purchased car, as you technically haven’t paid for it in full. So, if an individual fails to make the repayments over a certain period of time, the car can be repossessed by the lender.

How a fixed rate car loan works

Fixed rate car loans are the most common among car buyers, where the interest is calculated based on the principal amount borrowed and the length of the loan period. With this, your monthly instalment remains fixed from the start and stays that way until the end of the loan.

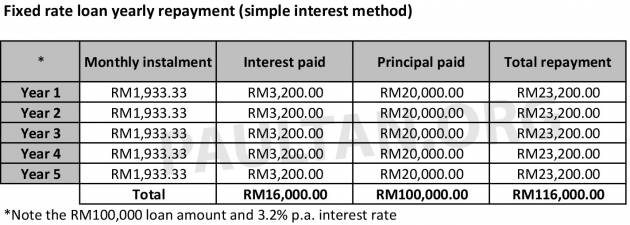

Let’s say you want to buy a car priced at RM115,000, and you already have RM15,000 ready for the downpayment. For the remaining RM100,000, you decide that you want a fixed rate car loan for a period of five years. In this hypothetical scenario and the others to come, for sampling purposes, we’ll use CIMB’s rate, which, at the time of writing is 3.2% per annum for fixed rate car loans.

With these parameters, the total interest you’ll have to pay will be RM16,000, which is calculated by multiplying the borrowed amount with the interest rate, followed by the number of years (RM100,000 x 3.2% x five = RM16,000). Adding the interest with the borrowed amount, the total amount owed to the bank becomes RM116,000, which, when divided by 60 months (five years), the monthly instalment amount is RM1,933.33.

With everything pre-calculated, it’s all rigid and your repayments do nothing to reduce the total interest you have to pay. This is why it’s always said that there’s no point paying more than the monthly instalment when servicing a fixed rate car loan, as the payment will merely be considered an advance for the following month. Say you finish paying a five year loan in two and a half years through monthly payments, you still pay for all the interest owed to the bank – in this case, the bank simply takes all the interest earlier.

Some banks do allow you to settle the loan early if you happen to have some extra cash on hand, although early settlements can be met with a rebate (or penalty in some cases) depending on the circumstances, so you’ll have to check with your bank before you decide to do so.

Simple interest versus Rule of 78 method for fixed rate car loans

While a fixed rate car loan appears to be a straightforward affair at first glance, there’s actually more to unearth. If we follow the simple interest method, the interest amount and principal paid remains the same throughout the loan tenure. The easy-to-digest approach means the RM1,933.33 instalment is split (with a bit of rounding) between repaying the principal amount (RM1,666.67) and the interest (RM266.67), both of which will remain the same throughout the loan period.

However, the reality is it’s not as simple as that. In most cases, banks in Malaysia use the Rule of 78 (also known as the Sum of Digits) method when computing the interest to be earned from providing car loans to borrowers.

This method of interest apportionment places higher interest charges in the early period of the loan and progressively reduces it towards the end of the loan tenure. This discourages borrowers from settling the loan early because the principal amount is still high, while helping maximise profits for the bank.

Our sample calculations show that in the first 12 months alone, you would pay RM5,718.03 in interest with the Rule of 78 method compared to the RM3,200 with the simple interest method.

Now, let’s assume after two years, you want to pay off the remainder of the loan, at which point you would have paid up RM36,222.95 for the principal amount. The remaining principal amount following the Rule of 78 method would be RM63,777.05 (RM90,000 – RM36,222.95) instead of RM60,000 with the simple interest method.

The difference isn’t huge, as you are paying the same amount month to month, and the total amount paid for both methods after five years are the same too. Where it does make a difference is if you decide to sell off the car and settle the loan before the tenure ends. Here, The Rule of 78 favours the bank rather than the borrower, as you’d owe a bigger portion of the principal amount.

Note that this is not something that you can choose or opt out of. It’s common practice for car loans in Malaysia. Not that you can do anything about it, but we thought you should know.

How a variable rate car loan works

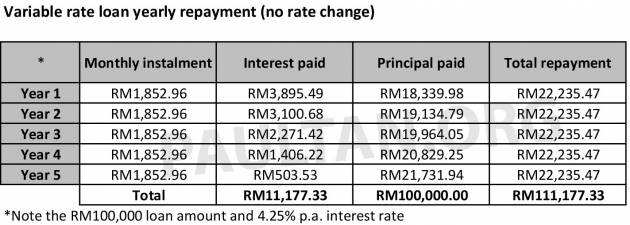

Compared to a fixed rate car loan, a variable rate car loan calculates the interest based on the base lending rate (BLR) stipulated by the bank. The rate is typical presented as “BLR +/- X.XX%” and is commonly higher than that of a fixed rate car loan. On CIMB’s site, the BLR as at July 13, 2020 is 5.6%, and the variable rate is listed as BLR – 1.35%, so the interest rate is 4.25%.

That doesn’t sound very encouraging compared to the 3.2% of the fixed rate loan we talked about earlier, but a variable rate car loan does have a unique aspect that some car buyers might find appealing. Unlike a fixed rate car loan, the interest is calculated based on the reducing balance method. With this, the interest is calculated over time based on the principal amount after deducting what you’ve paid, which is somewhat similar to housing loans.

The benefit is if you have some extra cash available, some banks provide you with the opportunity to reduce your interest by making extra payments toward the principal amount, which can also reduce the instalment amount for the following months. You’ll have to check with the banks to see if this is an option available to you.

This flexibility is not without its risks though, because if market conditions are not good and the bank decides to adjust its BLR and/or variable rate unfavourably, you could see your instalment amount increase. On the other hand, if the rate changes benefit you, the amount paid monthly goes down.

Recreating the abovementioned example, we’ll keep the borrowed amount (RM100,000) and loan tenure (five years) unchanged, while using CIMB’s rates. In this simulation, the BLR is 5.6% and the variable rate remains the same all the time at BLR – 1.35%, which gives us an interest rate of 4.25%.

If the BLR and variable rate remains the same for five years, the instalment amount remains unchanged, with the interest paid monthly gradually reducing as you pay off the loan, while the amount to pay off the principal amount rises.

Now, let’s assume the BLR is 5.6% in the first year and it goes up by half a percent in the second year to 6.1%, and again by 0.5% to 6.6% for the third year and staying put for the fourth and fifth year. With each BLR hike, the interest rate and interest payable go up together with the instalment amount, and the difference can be substantial. If the reverse happens where the BLR is adjusted downwards, you pay less.

Factoring in extra payments but keeping the BLR at 5.6%, you can see that the interest and instalment amounts go down. The best-case scenario is if you make extra payments and the BLR continuously goes down, which isn’t something that can – realistically – happen often.

The examples provided here are simplified and hypothetical models to illustrate the effect of variable rates and is based on our understanding on the matter (we’re sure the financial gurus out there can offer their insights in the comments). With the various rates offered by banks, it’s prudent to ensure you do your due diligence and get a clear understanding of your repayment schedule, be it with a fixed or variable rate car loan.

So, which is better?

Depending on what you want from your car loan, both fixed and variable rate car loans have their benefits. For those who prefer consistency and predictability, a fixed rate is the best option, as they know exactly how much they will have to pay monthly over the loan tenure. There are no surprises, no changes over time, nothing to catch you off-guard.

Meanwhile, those who prefer some flexibility and have the ability to fork out extra every now and then would find a variable rate to be beneficial, as you can potentially finish off your loan sooner and pay less interest. On the flipside, you’ll have to deal with commonly higher interest rates and possible BLR changes – good or bad – that come your way.

With loans, the longer the tenure, the cheaper the instalment, but you’ll have to pay more interest in the end, which is another thing to take note of. So, while a nine-year loan might be tempting, you could spend more to finance your new ride, which will invariably depreciate over time.

If you wish to change to a new car a few years down the line, you’d be far better off selling an existing car with one year of loan left compared to one with five years to go (i.e. four years into a five- or nine-year loan). Your car’s resale value would factor in heavily here too, but that’s a discussion for another time.

In the end, the type of car loan you take boils down to a matter of preference, but you should always do your research and check with your bank to ensure you are clearly informed before pulling the trigger. Do share your experiences with either fixed or variable rate car loans in the comments below, and point out anything of interest.

The post Fixed rate versus variable rate car loans in Malaysia – what’s the difference and which one should you pick? appeared first on Paul Tan's Automotive News.

0 Comments